Millennials & Gen Z: Rethinking Financial Security

The Millennial generation, which now represents the largest generation in the workforce, and their successors Gen Z, present an interesting lens into how perceptions of financial security have changed over time.

Early generations felt financial security was grounded in a long-term job with a large employer, benefits, possibly even a pension plan, and definitely Social Security (for those in the U.S.).

For Millennials, financial security looks a lot different. This generation crashed into the Great Recession, wage stagnation, student loan debt, and the rising cost of living. At the same time, the likelihood of Social Security seems to decline by the day, and pensions were often long gone before Millennials entered the workforce.

Even more interesting, perhaps, is that many of these differing generational experiences around financial security have occurred on opposite ends of the generational spectrum—yet may be represented in the very same family. Baby Boomers might be receiving retirement benefits and Social Security and had a chance to buy homes when they were more affordable relative to wages. However, their Millennial children may find those same pathways out of reach.

According to a recent report by Merrill Lynch Wealth Management, one thing these different generations do agree on is that financial success has nothing to do with being rich.

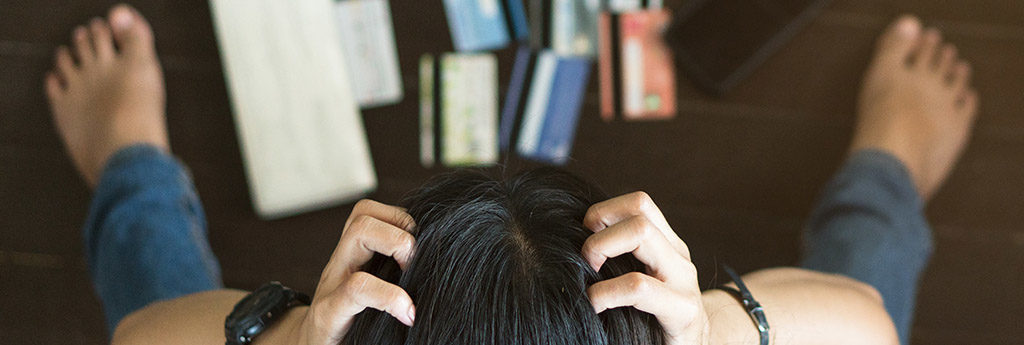

Our report asked more than 2,700 Americans ages 18-34: “How do today’s early adults define financial success?” Sixty percent say that it’s being debt free; only 19% say that it’s being rich. Freedom from debt seems a low bar of accomplishment, yet it’s an elusive goal for many early adults.

Financial freedom is not free

Why is that? I shared my research and insights on the unique and often polarized fiscal views of Millennials and Gen Z with Business Insider recently, which is why Mysanantonio.com came to me for insight into Merrill Lynch’s findings. Here are the thoughts I shared with them:

Older millennials graduated from college and entered the workforce during the height of the Great Recession and with considerable student-loan debt in tow. They delayed many of the traditional markers of adulthood, such as marriage, kids, and buying homes because of this.

And not just that. Millennials, struggling to pay off those student-loan debts (which MySanAntonio.com reports is at a national record level of $1.5 trillion) has kept them from saving as well.

The saving struggle is real

“Student debt is having major ripple effects on early adults’ futures, financially and personally,” the Merrill Lynch report said. “Four-hundred-thousand early adults who would have purchased a home a decade ago have not been able to afford one… and indebted graduates are contributing only about half the amount to their 401(k)s compared to those without debt.”

I agree wholeheartedly, and my research institution The Center for Generational Kinetics (CGK) has found the same to be true. CGK’s substantive research on the generation indicates older Millennials often realize they’re going to have to play catch-up with their finances if they ever want to be able to retire. In fact, some of them have already decided that they likely will not ever be able to afford to retire.

The weight of debt is real for the older members of the Millennial generation, which explains their aversion to debt. And, Gen Z (with their own student loans to contend with) watched their older peers struggle through the roughest part of the Great Recession, which explains theirs.

But it’s not all doom and gloom.

The need for Millennial change

As Millennials continue to get older, with the majority of them over the age of 30, studying and understanding their relationship with money, investing, and retirement planning has never been more important. This generation is poised to upend—and is already driving tremendous change—across banking, financial services, home buying, and many more categories.

This is why the team at CGK regularly leads deep-dive U.S. and global studies into the mindset of Millennials and money, including how they spend, save, invest, and influence financial institution trends and conversations.

The fact is, the Millennial and Gen Z generations are resilient, and they’re motivated to turn what has been a challenging intro to adulthood into a successful, financially stable future. The insights we’ve uncovered in our research at CGK tell me, without a doubt, that this generation is going to make that so.

Are you looking for a Millennial and Gen Z expert to help your organization and your employees understand generational financial nuances?

Please send an email, and my friendly team will provide information about my custom presentations, our Millennial and Gen Z research solutions, and my keynote availability. I am passionate about sharing our latest findings and strategies for engaging with each generation based on how they earn, spend, save, and invest!

Find me on Instagram (@Jason_Dorsey) to follow me as I share generational adventures from around the world.

Posted: July 1st, 2019

Categories: Gen Z | Investing | Millennials

Written by Jason Dorsey

Jason Dorsey is an acclaimed generations and behavioral researcher and speaker. He's received over 1,000 standing ovations for his unique keynote presentations. Jason has led over 120 research studies. Adweek calls him a "research guru." His mission is to deliver new insights and practical strategies that solve business challenges for leaders.